Market Outlook Newsletter

4th Quarter 2023

A near-term recession continues to be elusive as the employment market remains healthy and inflation continues to moderate.

Most inflation readings in Q3 point to a continuation of the downward inflation trend that has been in place since the recent peak in mid-2022. We will be watching to see how much the recent surge in oil prices offsets the likely moderation of inflation in housing. Volatility may continue in fixed income and equity markets, but long-term investors will benefit from higher interest rates and lower equity valuations.

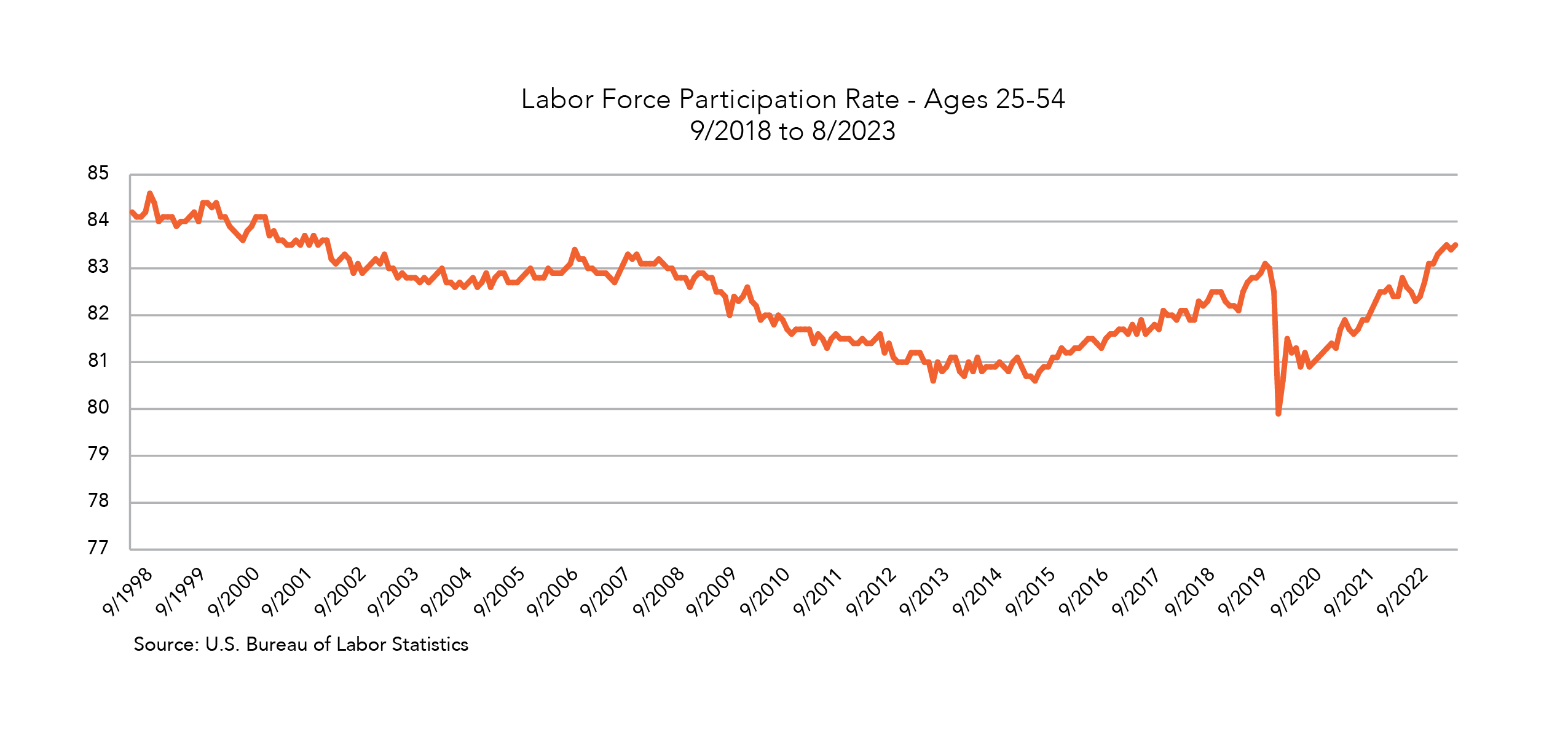

Nearly every recession in U.S. history was coupled with a deteriorating employment market. That is why we monitor the employment trends closely. While there have been a few headline-grabbing layoff announcements over the past year, most have been isolated to a handful of technology companies that had been aggressive with their hiring trends in years prior. According to the monthly U.S. Nonfarm Payroll data, there are more than 1.8 million more people working as of August 31 compared to the beginning of the year. While most people are returning to the workforce to fill open roles, some may be reentering due to recent high inflation impact. The labor force participation rate for those 55+ years old remains low following the pandemic, indicating that most early retirees continue to stay in retirement. Meanwhile, higher wages seem to be drawing younger workers back into the labor pool. The labor force participation rate for people between 25-54 years old is up to 83.5%, the highest level in over 20 years. It may soon be more challenging to see additional gains in net employment numbers unless some early retirees are drawn back into the labor pool.

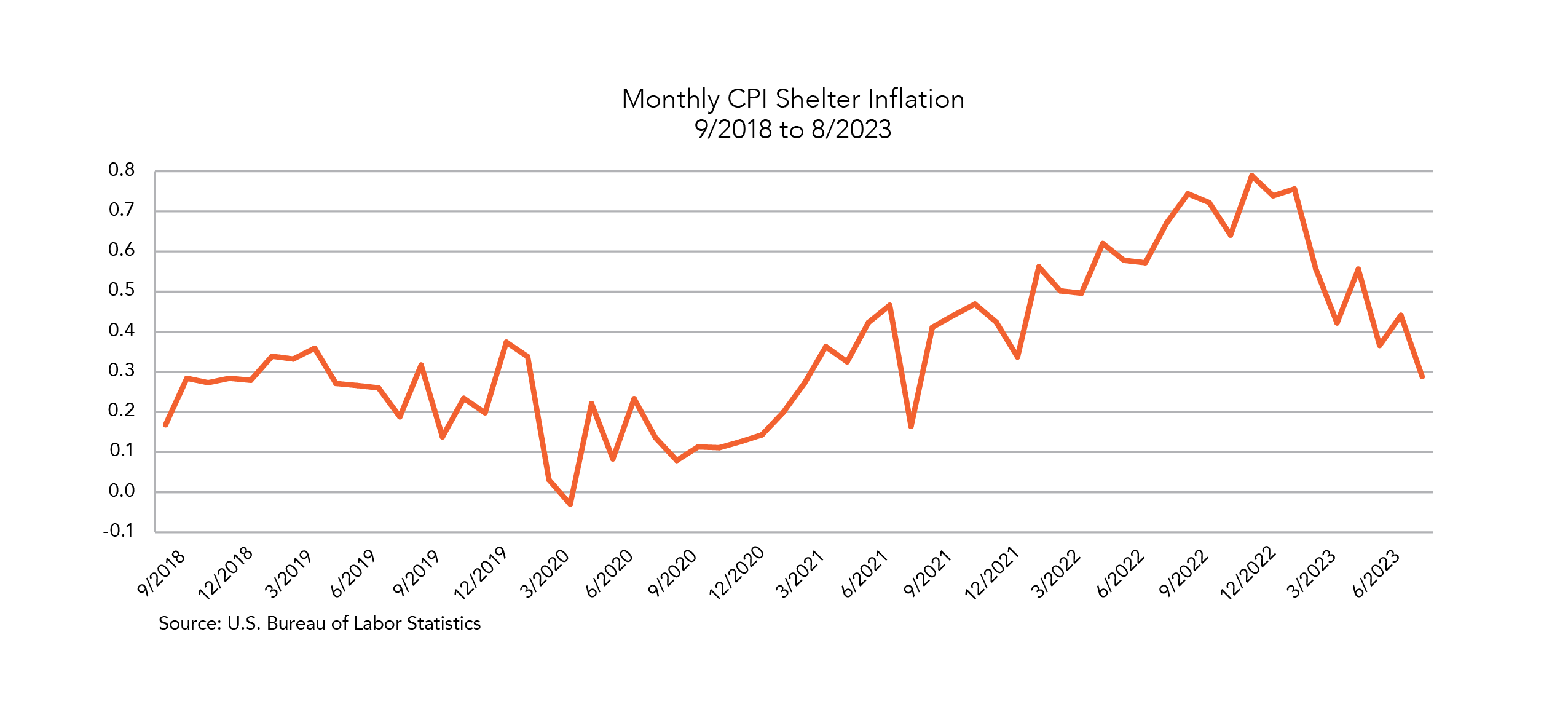

Investors remain focused on when the Federal Reserve (Fed) will be done raising the federal funds rate, and more importantly, when they may start to cut rates. The key will be the future path of inflation. While the Consumer Price Index (CPI) seems to remain sticky above 3%, it is also important to monitor which segments of the economy are pushing inflation higher. Following the immediate impact from the pandemic in 2020, inflation started to show in physical goods such as lumber, vehicles, and electronics due to production bottlenecks. Then in late 2021 and into 2022, inflation shifted toward various parts of the service-oriented segments of the economy as people started spending more outside of their homes again. As inflation has been moderating in the services sector recently, it has shifted toward higher levels of inflation in shelter over the past year. This is important because shelter, comparable to monthly cost of housing, makes up more than 1/3 of the total CPI index. It is also important to factor in that the shelter component is measured on a lag. The monthly increases in shelter inflation recently peaked in late 2022 to early 2023, which will be rolling off over the next 6-months when looking at year-over-year CPI data. This should help the broad inflation data to continue to moderate unless a new segment of the economy starts to see renewed inflationary pressure.

If inflation data continues to moderate in the months ahead, it should give the Fed the opportunity to slow down additional monetary tightening. More stable interest rates may provide renewed support for the equity market.

VOLATILITY MAY CONTINUE IN FIXED INCOME AND EQUITY MARKETS, BUT LONG-TERM INVESTORS WILL BENEFIT FROM HIGHER INTEREST RATES AND LOWER EQUITY VALUATIONS.

Midland Wealth Management is a trade name used by Midland States Bank, Midland Trust Company, and Midland Wealth Advisors, LLC, a registered investment adviser. Investments are not insured by the FDIC or any other government agency, are not deposits or obligations of the bank, are not guaranteed by the bank or any federal government agency, and are subject to risks, including the possible loss of principal. The information provided is for informational purposes only. Information has been obtained from sources believed to be reliable, but its accuracy and interpretation are not guaranteed. Midland Wealth Management does not provide tax or legal advice. Please consult your tax or legal advisors to determine how this information may apply to your own situation. Whether any planned tax result is realized by you depends on the specific facts of your own situation at the time your taxes are prepared. IRS CIRCULAR 230 NOTICE: To the extent that this message or any attachment concerns tax matters, it is not intended to be used and cannot be used by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Past performance is no guarantee of future results. Returns of the indexes also do not typically reflect the deduction of investment management fees, trading costs or other expenses. It is not possible to invest directly in an index. Indexes are the property of their respective owners, all rights reserved. Midland Wealth Management does not claim that the performance represented is CFA Institute, GIPS, or IMCA compliant. Copyright © 2023 Midland States Bancorp, Inc. All rights reserved. Midland States Bank® is a registered trademark of Midland States Bancorp, Inc.

By Mark Votruba

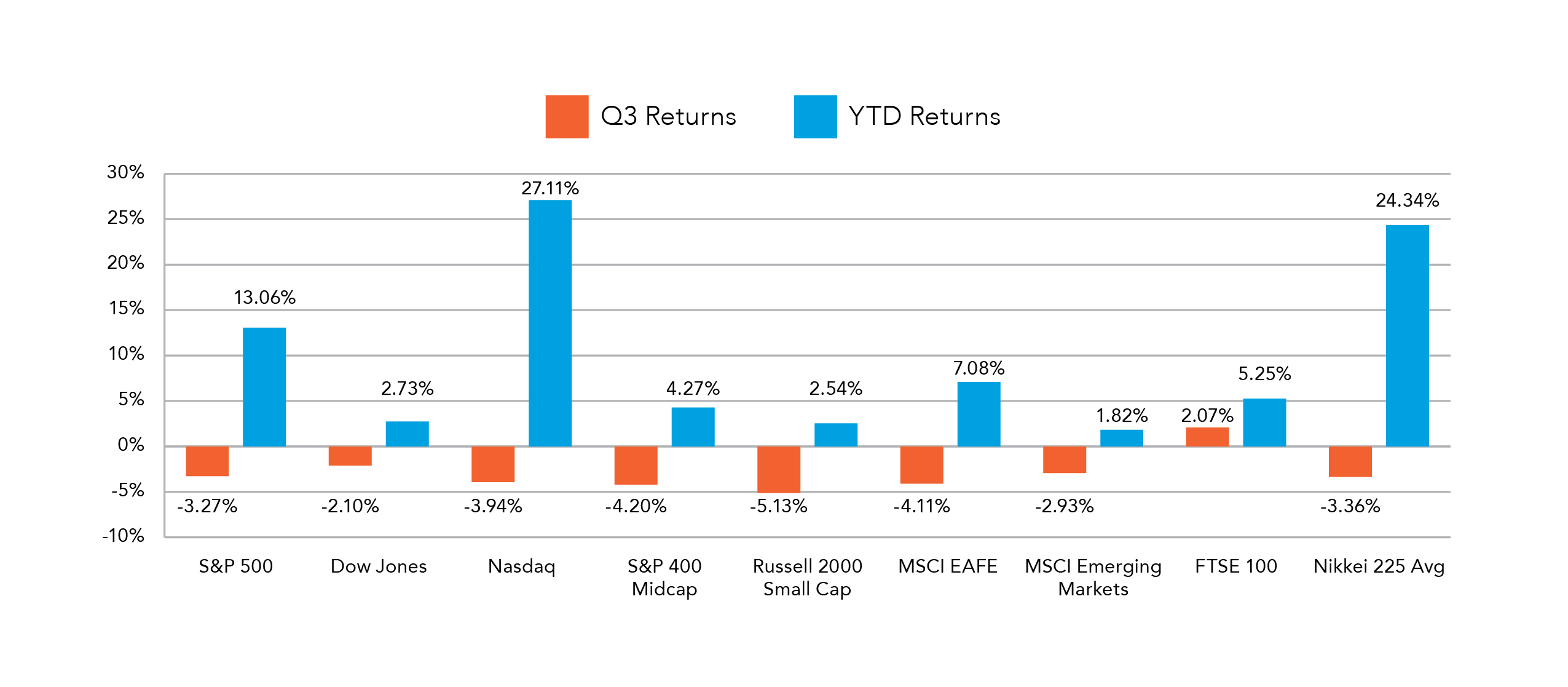

Equity markets stumbled during Q3 as the S&P 500 fell by more than 3%, yet remains well into positive territory for the year, up more than 13%.

Our neutral outlook for equities remains in place while maintaining a defensive tilt to our positioning as we enter the final quarter of 2023.

The performance for Information Technology was in the bottom third of all S&P 500 sectors during Q3, with eight of eleven industry groups finishing in negative territory. While the index remains firmly in positive territory for the year, the gains are still largely attributable to optimism surrounding Artificial Intelligence and the handful of mega cap holdings that have an outsized influence on the index return. One of these names, Apple Inc. (AAPL), was down more than 11% as China placed restrictions on the use of iPhones by some government agencies, which led to speculation that further restrictions on the company’s flagship revenue driver could be forthcoming. Despite slowing momentum behind the AI trade during Q3, the space appears crowded and richly valued as investor sentiment for the group remains optimistic as we approach 2024.

September has historically been one of the toughest months of the year. The trend continued in 2023, with the S&P 500 posting back-to-back monthly declines, a feat not accomplished since the same period of 2022. Several factors converged during Q3 creating a headwind to equities. A combination of the UAW strike and the threat of a government shutdown, together with the resumption of student loan payments and the 30% jump in oil prices converged to weaken investor sentiment. Taken individually, none of these factors would pose a significant hurdle to the outlook for equities but together have conspired to construct a wall of worry as we approached quarter end. Although GDP growth continues to track above expectations, the Federal Open Market Committee’s (FOMC) efforts to stifle inflation will, in theory, work to slow economic expansion. The U.S. 10-year Treasury yield moved steadily higher during the quarter, finishing above 4.5%. Elevated long-term yields and the Fed’s higher-for-longer stance on short-term rates will work together to challenge valuations and pose a headwind to equity markets. Although rates have been a challenge, if growth were to slow with inflation continuing to moderate, a pause and eventual reversal of FOMC policy would in turn signal rate relief, a theoretical tailwind for equities. The outlook toward a soft landing for the economy has helped keep the S&P 500 well into positive territory, up 13% year-to-date. Whether we can navigate a slowdown in economic activity and corresponding inflationary pressures without tipping into recession will be a focus of investor sentiment as we approach year end.

International markets were also largely negative during the third quarter as well. London’s FTSE 100 Index did manage to stay in positive territory during Q3, deviating from much of the developed markets, as valuations in Europe continue to look inexpensive. Higher-for-longer rates have had more of an impact on the European economy with GDP growth stalling, posing a potential challenge to equities as we enter the final quarter of 2023. Japan’s Nikkei has led major world indices year-to-date, up more than 24% and 11% over the S&P 500. A combination of sustained U.S. growth and corresponding higher rates have kept the U.S. Dollar strong relative to the Japanese Yen, which is beneficial to Japanese equities. With the potential for an end to negative interest rates in Japan, 10-year JGB yields moved into positive territory at 0.7%, the highest in nearly a decade. The possibility of yield curve control coming to an end in Japan should continue to be a tailwind for the country’s financial stocks and another potential positive for the Nikkei Average into next year.

THE OUTLOOK TOWARD A SOFT LANDING FOR THE ECONOMY HAS HELPED KEEP THE S&P 500 WELL INTO POSITIVE TERRITORY...

By Betsy Pierson, CFA

With the increase in interest rates, bonds offer value to investors not seen in 15 years.

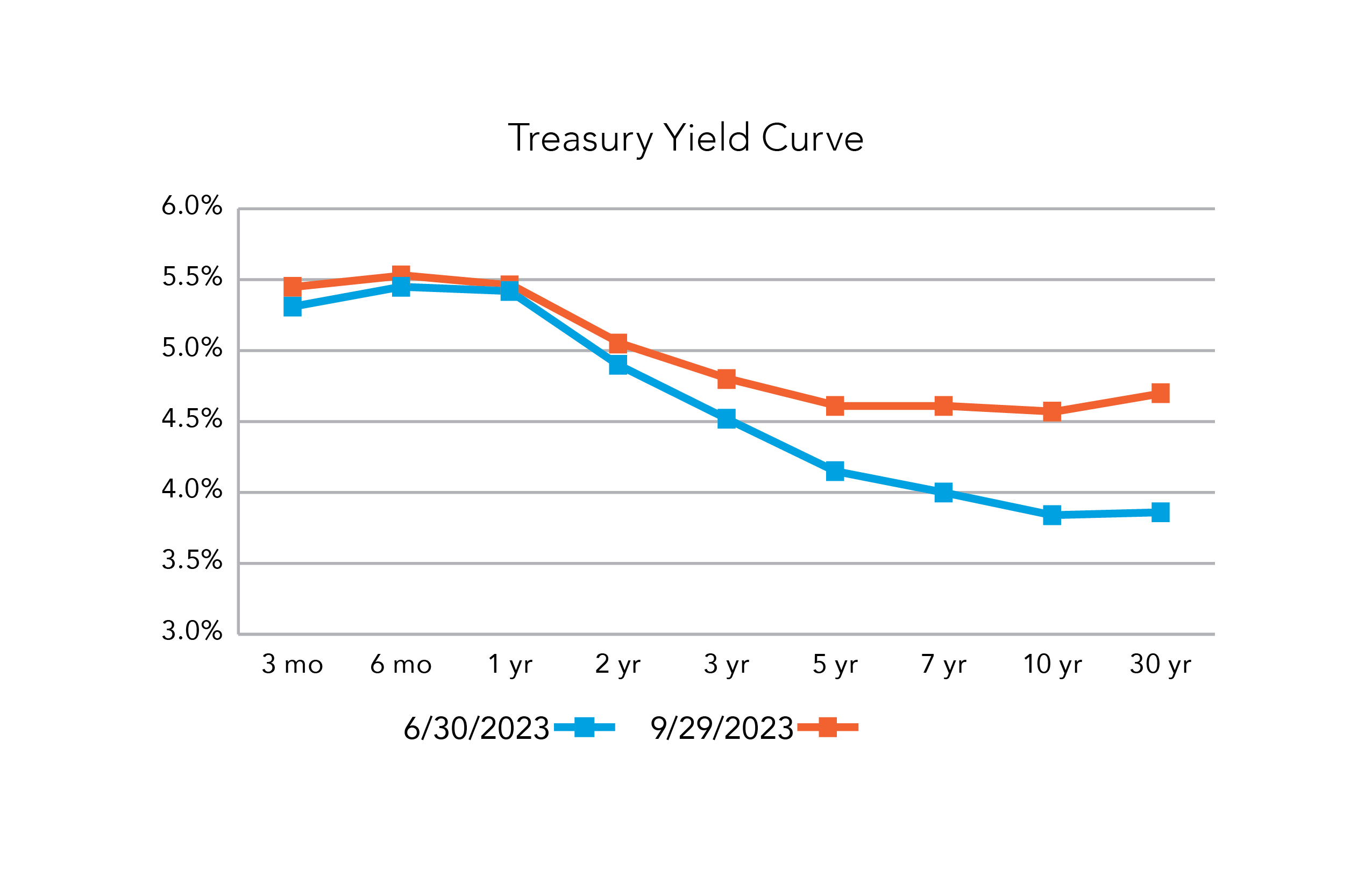

While inflation continues to decline from its highs in mid-2022, the FOMC continues to be diligent in its fight to bring it back to its target rate of 2%. At its July meeting, the overnight rate was increased from 5.25% to 5.50%, which was a highly anticipated move. At the most recent meeting in September, there was no change to the overnight rate, but the comments following the meeting put pressure on intermediate- and long-term rates.

The comments following the meeting focused on holding steady for now and potentially implementing another rate increase in the future. From the FOMC’s perspective, rates will remain higher for longer. While we were not surprised by this commentary, the market responded with a spike in treasury yields, especially in maturities longer than two years, with the largest move in the 10-year maturity (see yield curve chart). It increased over 0.70% during the quarter and reached a yield level not seen since the early 2000s.

Along with the comments by the Fed, the fear of increasing issuance by the Treasury to cover the ever-growing deficit and debt levels, as well as the climbing interest expense, also contributed to higher rates. The level of government debt issuance each month is gradually increasing. One of the primary buyers, the Fed, has cut back on the amount of bonds being purchased compared to the level seen during the pandemic as it attempts to unwind the excess stimulus. More supply and less demand lead to higher yields.

We do believe the FOMC should hold rates at these levels and not implement any further tightening, but the path will depend on future economic data. Inflation is moving lower, the employment market is trending to a more balanced position, and mortgage rates have moved high enough to slow down the housing market. If these trends continue, they will provide support to maintaining the current rate level.

While it is painful when interest rates increase and overall returns are negative, it does provide an opportunity for investors to put funds to work in intermediate- and longer maturity investments. As interest rates have risen during the quarter, our Investment Strategy committee increased exposure to intermediate treasuries and overall fixed income. At this time, this move may seem premature to the average investor since money market rates are equal to or slightly higher than the rates on longer maturity investments. While money market rates are currently equal or slightly higher, when the FOMC or market indicates the next move is lower in the overnight rate, short-term yields typically decline much more rapidly than intermediate-term yields. In that environment, investors that have extended maturities and locked-in yields will be rewarded.

By Ronald Glenn, M.A., CFP®

Did you know that October is Cybersecurity Awareness Month? It’s true – since 2004, the President of the United States and Congress have declared October as a month dedicated for the public and private sectors and tribal communities to work together to raise awareness about the importance of cybersecurity. The task seems daunting – where does one begin, what is most important to consider, and what is the most effective strategy for keeping oneself safe in our ever-increasing digital world? Should we ditch the cell phone, return to the landline, and illuminate our houses at night with candles? I am being facetious, of course, but it does seem like eliminating the device itself solves all our problems, but then others are likely to bubble up. Here are some things to consider during this month (or any month), with the caveat that I am merely scratching the surface.

Don’t balk at the suggestion or the opportunity to double your login protection when it’s available. No matter how long and strong your password is, a breach is always possible. All it takes is for one of your accounts to be hacked and your personal information and possibly other accounts can be accessible to cybercriminals. If you enable multi-factor authentication, the only person with access to your account information is you. Use it for banking, social media, email, and any other service that requires logging in.

Practice safe surfing wherever you are by checking for the green lock or padlock in your internet browser bar – this indicates a secure connection.

Whenever you are out and about, avoid free internet access without encryption. If you do use unsecured Wi-Fi, avoid banking or any kind of financial transaction or activity, including using a credit card for shopping or service purchases.

Seemingly real emails from known institutions or business contacts may ask for financial or personal information. Cybercriminals will often offer a financial reward, threaten you if you don’t engage, or claim a family member is in dire need of help.

If they have any details from your life – your job title, email address, full name, and more that you may have published online somewhere – they can attempt a phishing attack on you. Cybercriminals can also use social engineering with these details to try to manipulate you into skipping normal security protocols. If you’re unsure of the email sender, even if details seem accurate, don’t respond or click on any links or attachments found in the email.

Let’s face it – we’re inundated with reminders, alarms, and interruptions throughout the day. The to-do list seems to grow faster than the completed list. We can easily let our guard down and find ourselves susceptible to security breaches in our offices and homes. Slowing down and visualizing the online criminal intent on wreaking havoc on your digital life seems to be the order of the day.

Our team of dedicated professionals are here to support you.